Fundraising Case Studies

Nic Mahaney

Prev. OnePager Co-Founder

September 7th, 2021

Bootstrapping

What is a Bootstrapped Startup?

Bootstrapping in business means starting a business without the help of any outside capital such as venture capital and angel investment and growing it internally using limited capital (Harvey).

Rather than seeking outside capital, founders of bootstrapped startups usually rely on their personal savings, debt, and/or funding from friends and family for initial capital (Pujji). A bootstrapped startup usually grows through three stages of funding: 1) beginning stage, 2) customer-funded stage, and 3) credit stage. In the beginning stage, the startup relies on the founder’s personal income, savings, debt, or funding from friends and family. In the customer-funded stage, payments from customers are able to support the operation of the startup and possibly fund its growth. In the credit stage, in order to fund specific business activities (e.g. improving equipment and hiring staff), the startup takes out loans or may begin to start looking for outside investment for expansion (Harvey).

Many successful businesses were bootstrapped until they reached sizable revenue figures and grew to hold powerful positions within their industry; only since then have they raised outside capital. This allowed them to easily attract outside investors and even negotiate for better terms in the credit stage (Kuppusamy). Here are some examples of successful businesses that started out as bootstrapped startups:

Successful Bootstrapped Companies

Here are some examples of successful businesses that started out as bootstrapped startups:

- GoPro is an American technology company that manufactures action cameras and develops its own apps and software. Nick Woodman launched GoPro in 2002 using his personal savings and $35,000 loan from his mother after his two previous businesses went bust. Woodman bootstrapped GoPro until 2012, when Foxconn invested $200 million. GoPro has since consistently grown revenue and went public in 2014, with an IPO valued at $2.96 billion (Gonzalez).

- GitHub is an American software company that offers a web-based hosting service for software development projects. Tom Preston-Werner, Chris Wanstrath, and PJ Hyett launched GitHub in 2008, spending only a few thousand dollars by working remotely. The founders bootstrapped the company until it received a $100 investment from Andreeseen Horowitz in 2012. Since then, GitHub has raised over $250 million from other outside investors, and a funding round in 2015 valued the company at $2 billion (Gonzalez). GitHub currently has over 40 million registered users worldwide (Harvey).

As evident in the above examples, bootstrapping a startup, if successful, can bring increased margins than raising outside capital from the beginning. However, it also has downsides. It is therefore crucial for founders to thoroughly understand the trade-offs. Firstly, the advantages of bootstrapping a startup include:

Advantages of Bootstrapping a Startup

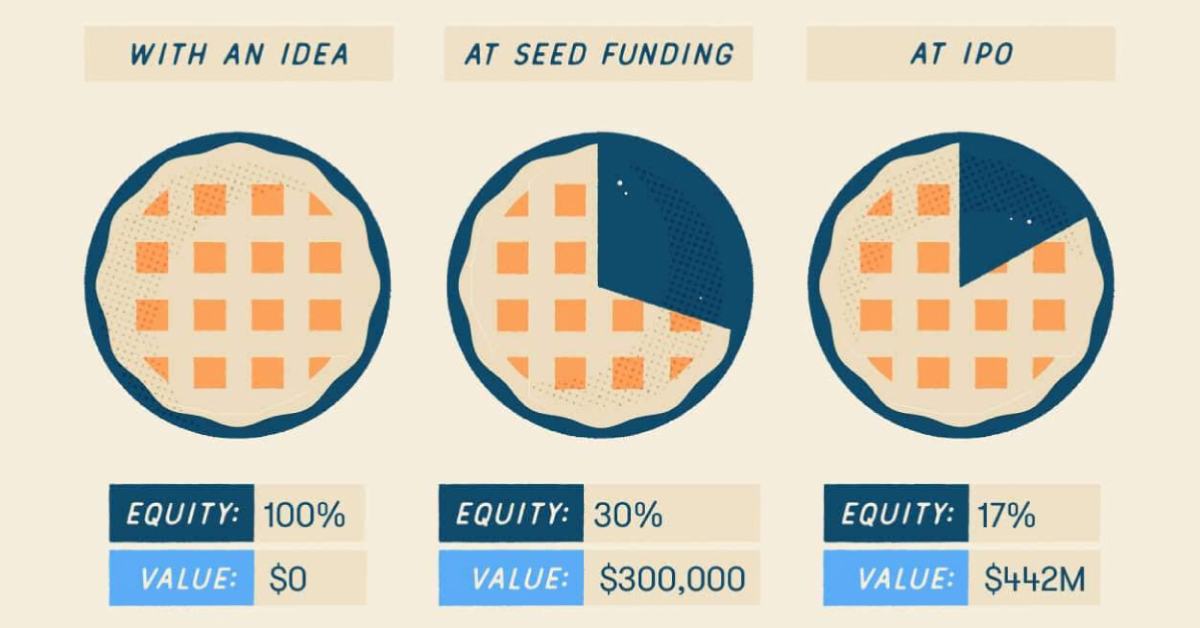

- Founders retain full ownership. Even with a much smaller business, the founder’s equity may be worth more than if he/she raised outside capital to achieve a higher valuation (Cremades). Even if the startup ends up receiving outside investment in future, bootstrapping would allow the founder to preserve his/her equity until the startup holds a powerful position within its industry and the founder is therefore able to negotiate a better price for his/her equity (Kuppusamy).

- Founders retain full control over their startups. Since there is no exterior pressure or external party such as outside investors involved, founders can decide the direction of their startups without having to convince or negotiate with anyone. They can execute their plans and make any changes at their own speed (Philemon)(Pujji).

- Bootstrapping provides founders with an opportunity to build a life-time or multigenerational business. In many cases, outside investors ask for or force the sale of their portfolio businesses within about 10 years to achieve a sizable exit (Cremades).

- Founders are forced to try monetizing their startups early in order to fund their business activities without outside capital (Rice). Iterating their ideas to real market demand allows founders to test how well their ideas work and whether their current business models are sustainable at an early stage (Rice). This also means that customers take center stage for bootstrapped startups. While many externally financed startups build products/services that their investors or boards want them to build, bootstrapped startups are forced to focus on customers’ needs in order to instantly generate positive cash flows and profits (Pujji).

- The exit process for founders tends to be more simple for bootstrapped businesses since there are no competing interests to negotiate (Philemon).

Disadvantages of Bootstrapping a Startup

- Bootstrapped startups have a lower chance of survival. One of the most common reasons for startup failure is cash flow shortages; many startups fail before even realizing their potential because they simply cannot afford to stay afloat (Cremades). Lack of capital can also limit the flexibility of startups which is often directly related to their survival (Pujji). For example, if a bootstrapped startup suddenly loses its biggest client whose payments it has relied on to fund its business activities, the startup may suffer greatly, without any external capital to financially support its daily operation. This would also have a negative impact on the startup’s employees and customers. If the startup does not recover financially and eventually fails to survive, its employees would lose their jobs and its customers would have to look for other companies that provide similar products/services.

- Lack of capital can limit the future growth of startups. Without outside capital, founders have limited options and resources in terms of marketing, customer services, product development, hiring etc, which may hinder their startups from reaching their potential (Cremades). For this reason, in a competitive industry where businesses need to keep up with constantly rising standards, bootstrapped startups can even end up struggling for survival, let alone expand (Riani).

- Founders usually have little to no access to top level guidance or support. Outside capital often brings top level guidance and support from outside investors as well (Cremades). However, bootstrapped startups cannot enjoy such benefits. This means that, if a founder does not have all the necessary skills, knowledge, and experience to grow his/her startup independently , the business is likely to face many challenges (Philemon). Also, without top level guidance and support from outside investors, founders sometimes must personally reach out to experts in their industry for help, which may require a significant amount of time and effort (Pujji). They also do not have the pressure to succeed created by outside funding.

- Founders of bootstrapped startups need to work more hours and manage more roles since bootstrapped startups operate in a lean manner, with minimal resources and staff. For example, in addition to executing big ideas for their startups, founders may also need to take care of basics such as bookkeeping and taxes.

“Go big or go home”

Outside capital is any capital acquired from sources outside the company. There are various external sources of capital: equity capital, preferred stock, debentures, term loans, bank overdraft, etc. However, this particular section mainly focuses on venture capital.

Venture capital is a type of financing in which wealthy investors provide capital to startups and small businesses that they believe to have potential for long-term growth. Many of the multinational companies that we all know of have raised venture capital in their early years to establish and expand themselves in their respective industries. Here are some examples of successful businesses that have raised venture capital:

- Uber is an American ride-hailing company that offers services such as ride hailing, peer-to-peer ridesharing, and food delivery. Soon after its launch in 2009, Uber captured the attention of venture capital firms in the Silicon Valley and its total funding reached $10 billion in 2015, with Google Ventures investing over $250 million. In 2019, its initial public offering (IPO) valued the company at $82.4 billion (Vita).

- Meituan Dianping is a Chinese online services company that offers a broad range of services including movie ticketing, food delivery, ride hailing, and travel booking. Since its founding in 2010, Sequoia Capital China has invested over $400 million in the company and also helped coordinate the crucial merger between the company and its then rival Dianping in 2015. In 2018, Meituan Dianping raised $4.2 billion via its IPO, valuing the company at around $52.8 billion (Lau).

Although the above examples highlight the power of venture capital, not all companies backed by venture capital have turned out to be successful. Many of them failed even after raising millions due to various reasons: low market demand, intense competition, faulty product/service/business model, etc. Below are some examples:

- Jawbone was an American consumer electronic and wearable products company that manufactured bluetooth earphones, wireless speakers, and fitness trackers. Although it had promising products and raised around $930 million from leading investors such as Sequoia, Andreessen Horowitz, and Khosla Ventures, it struggled to compete against its giant competitors such as Fitbit and Samsung that came into its niche markets later, and it eventually ceased its operations in 2017 (Maurya).

- Vreal was a game-streaming platform that aimed to allow VR users to explore the virtual worlds in which live-streamers were playing. Despite raising around $15 million from investors such as CRCM Ventures, Vreal shut down in 2019 because the VR market did not grow as quickly as they expected (Heater).

As the above examples suggest, raising a lot of venture capital does not always guarantee success for startups. In fact, the failure rate among venture capital-backed startups has been on the rise lately (Maurya). It is therefore crucial for founders to keep in mind that, while raising a lot of venture capital can be perceived as a proof of a startup’s potential, a startup’s success depends on its actual performance (i.e. sales and profitability). Founders should also fully understand the advantages and disadvantages of raising venture capital before they decide whether or not its useful for their own startup. Firstly, the advantages of raising venture capital include:

Venture Capital Advantages and Disadvantages

Founders should also fully understand the advantages and disadvantages of raising venture capital before they decide whether or not it’s useful for their own startup.

Advantages of Raising Venture Capital

- Venture capital usually allows founders to preserve their own financial resources such as personal savings for other purposes than business operations.

- Venture capital allows startups to finance growth projects/strategies that they cannot fund on their own. For example, if a startup needs additional manufacturing equipment to keep pace with demand, outside capital can provide the necessary fund (Root). Such access to adequate funding is critical since speed of iteration is often one of the key factors for a startup’s survival and success (Rice). Also, since many growth projects/strategies focus on product development and customer service, outside capital can have a positive impact on customers as well.

- Investors are often a useful source of expert advice and guidance for founders in addition to capital. Experienced investors often provide their portfolio startups with valuable advice, such as guidance on how to avoid pitfalls that created problems for other startups they previously invested in (Root). They can also add value to their portfolio startups by connecting the founders with their network, which can make future rounds of funding easier.

- Startups backed by well-respected venture capital companies are generally viewed more favourably by customers and employees. Venture capital is often perceived as a proof of a startup’s potential, financial capability, and the founder’s dedication to building a successful business, given the effort raising outside capital requires (Kuppusamy)(Riani). Thus, it helps attract employees, customers, and investors in future rounds of funding as well as increases future acquisition chances.

Disadvantages of Raising Venture Capital Include:

- Pursuing venture capital requires a lot of time and effort, and there is no guarantee that founders will successfully raise it. One round of venture capital funding process which usually includes identifying and contacting potential investors, preparing and presenting a business plan, attending meetings, etc. can take possibly 10 to 20 man months (Kuppusamy). This can be very demanding for founders who have other important tasks to tend to such as developing their products/services, marketing, and hiring staff (Prosser).

- Raising venture capital requires founders to give up some of their control and ownership in their companies. Taking on venture capital funding also means taking on business partners; investors often obtain the right to vote on key decisions of their portfolio companies, which might compromise founders’ visions (Root).

- Some investors only care about their own interests. Since most investors want their portfolio companies to increase their revenues as soon as possible, founders can be urged to expand their teams, office space, or product lines before they feel ready to do so in order to satisfy their investors’ interests (Berry). Some investors may even try to position their portfolio companies to sell, regardless of founders’ visions, so that they can receive their return on investment quickly and move on to other companies (Prosser).

- Venture capital-backed companies can sometimes be so focused on satisfying their investors and boards that they end up building products/services their investors or boards want them to build, rather than what their customers want (Pujji).

Deciding Between Bootstrapping and Raising Outside Capital

Before deciding whether to bootstrap or raise outside capital, founders should take many factors into consideration. Some important factors include: uniqueness of the product/service, maturity of the market, pace of the startup’s current growth, length of the opportunity growth, and types of growth challenges and limitations.

However, founders are likely to be biased about the uniqueness and potential of their products/services, and outside capital may appear to be the solution for all of their problems (Kuppusamy). This could hinder them from making the best possible decision, so receiving advice from other founders with experience in both bootstrapping and fundraising can be helpful.

Although many startups have factors that can help them thrive without any outside capital, such as a strong position in a niche and industry relationships, there are some cases in which raising outside capital is necessary for startups (Rice). Below are some examples:

- If the only way to survive and thrive is to be the first mover in the industry and to create a network effort, or dominant brand, before any other company (Rice).

- If there has been a rapid change in technology, forcing the startup to invest large amounts of capital in technology to stay competitive (Cohan).

- If the startup is facing intense price competition which will eventually make the startup suffer from lower cash flows (Cohan).

- If the startup just lost its client whose payments it has relied on to fund its business activities (Cohan).

- If the startup’s value proposition is built on providing a secure and dependable long-term relationship for the client, which means the startup needs a strong balance sheet and possibly even well-known investors in order to convince its potential clients that it will stay in the industry for a long time (Rice).

Additionally, founders may find this score sheet made by Kuppusamy to be a useful tool for deciding between bootstrapping and raising outside capital. It has a series of questions regarding a startup and different points associated with them (Kuppusamy). Kuppusamy suggests that if a founder scores below 30, he/she should consider bootstrapping and if he/she scores above 40, he/she should consider seeking venture capital (Kuppusamy).

Creative strategies

Besides bootstrapping and traditional sources of outside capital such as venture capital, there are many alternative types of financing, and some of them are relatively new. This section focuses on the following alternative financing options: initial coin offerings, crowdfunding, accounts receivable financing, and revenue-based financing.

Initial coin offering

An initial coin offering (ICO) is the cryptocurrency industry’s equivalent to an initial public offering (IPO) (Frankenfield). A company looking to raise capital to create a new coin, application, or service can launch an ICO. Interested investors can then buy new cryptocurrency tokens issued by the company (Frankenfield). However, these tokens do not give investors any equity stake in the company. Instead, they can be used on the company’s upcoming product or service. Investors can also trade the tokens for profits if their value increases (Kharpal).

To launch an ICO, a company should create new cryptocurrency tokens first, which can be done via different platforms such as Ethereum, which provides companies with a toolkit for creating digital coins (Kharpal). According to Platform Review, Ethereum is the most popular platform used to issue ICO tokens; over 82 percent of ICO projects issue their tokens on Ethereum. Around 9 percent of ICO projects develop their own custom Blockchain platform for different purposes. Waves, NEO, NEM, and Stellar are some of the other popular ICO platforms that have had at least several successful ICOs held on them (CoinTelegraph). Also, the company usually needs to create a white paper outlining what its project is about, how much money it needs, what type of money it will accept, how long the ICO campaign will run for, etc (Frankenfield). In most cases, tokens are purchased with pre-existing cryptocurrencies such as Bitcoin or Ethereum (Kharpal). If the funds raised through an ICO are below the minimum amount required for the company’s project, they may be returned to the investors and the ICO is deemed unsuccessful (Frankenfield).

Many blockchain technology startups are now turning to ICOs instead of traditional forms of financing such as venture capital (Kharpal). An MIT Sloan assistant professor Christian Catalini, who has expertise in blockchain technologies and cryptocurrencies, estimates that “blockchain-based startups have raised over $8 billion through initial coin offerings since 2017, which far surpasses the $1 billion in traditional venture capital within the same sector” (Vereckey).

ICOs are largely unregulated in the US (Frankenfield). However, the Securities and Exchange Commission (SEC) can always intervene; if a new coin is deemed a “security”, then the company may have to register with the SEC (Kharpal).

Advantages of Initial Coin Offerings:

- ICOs are a relatively quick and easy way to raise capital. For example, it can take less than 100 lines of code to generate a token on top of Ethereum, and there are many online services that allow startups to generate tokens in a matter of seconds (Vereckey) (Frankenfield). Also, unlike IPOs, ICOs do not require any paperwork (Rosie).

- Successful ICO campaigns usually generate buyer competition for the token. This provides founders with an insight on real market demand (i.e. how much consumers are willing to pay for their service) (Vereckey).

- ICOs have the potential for very high returns for investors. If a startup’s project succeeds after its ICO launch, the value of its tokens purchased by investors will increase drastically. For example, NEO (previously known as Antshares)’s ICO raised around $4.5 million and provided exceptional returns on investment for its early investors; its price was $0.03 during the ICO but reached $10.74 at its peak (Frankenfield).

Disadvantages of Initial Coin Offerings:

- Due to the lack of regulations, founders do not have much clarity as to what they can and cannot do (Vereckey).

- Due to the lack of regulations, ICO campaigns are rife with scams and there is little investor protection. For example, A project named Giza claimed to be developing a secure cryptocurrency storage device and raised over $2 million from over 1,000 investors. However, it turned out to be a scam; the scammers eventually ran off with the raised funds without delivering any product (Kharpal). Since there is no paperwork required from founders, funds lost due to fraud or incompetence may never be recovered, investors must be cautious and do thorough diligence before they invest in a project to ensure the credibility of the founder and his/her team (Frankenfield).

- Investing in ICOs can be very risky because it is investing in products/services that do not exist yet. ICOs have very high failure rates; hundreds of coins have already failed and many of them were scams or did not materialize (Kharpal).

Successful Initial Coin Offering Examples:

- The early pioneer Ethereum’s ICO in 2014 raised $18 million in 42 days. Etheruem was priced at approximately $0.30 at its launch, but it is now priced at thousands of dollars (Frankenfield). Ethereum is currently the second-largest cryptocurrency platform by market capitalization behind Bitcoin.

- Filecoin, a decentralized cloud storage project, raised $257 million during its one-month ICO in 2018 (Kharpal).

Crowdfunding

Crowdfunding is another popular method for raising funds for businesses, enabling money to be raised through online platforms.

What is Crowdfunding and How Does it Work?

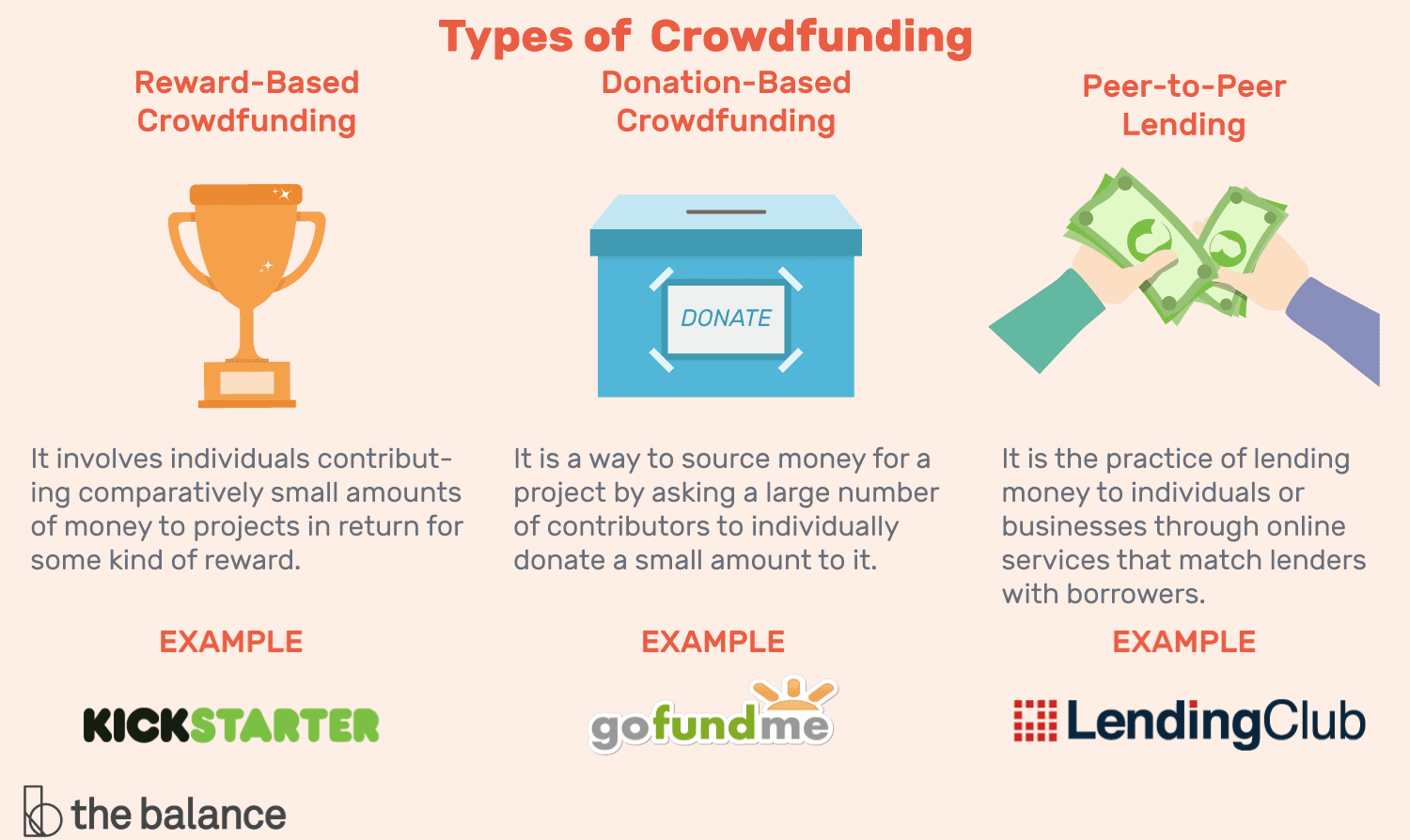

Crowdfunding is a fundraising method in which founders raise capital from a large pool of individuals using social media and crowdfunding platforms (Smith). There are a variety of crowdfunding types, but the three primary categories are: donation-based, rewards-based, and equity-based crowdfunding (McGowan).

Firstly, donation-based crowdfunding is any crowdfunding that does not offer any financial return to the investors, such as fundraising for charities and non-profits (McGowan).

Secondly, rewards-based crowdfunding allows investors to receive a small gift from founders in return for their investment (e.g. advance copies of a new video game to those who invested in the video game startup)(Smith). Some popular rewards-based crowdfunding platforms include: Kickstarter and Indiegogo (Nguyen).

Advantages of Rewards-Based Crowdfunding:

- Rewards-based crowdfunding allows founders to raise capital without giving up any equity (i.e. ownership) in their company.

- Rewards-based crowdfunding allows founders to build relationships with enthusiastic supporters in early stages, which can make future rounds of funding relatively easy (Miller).

Disadvantages of Rewards-Based Crowdfunding:

- On some crowdfunding platforms, founders do not receive any funding if they do not meet their target amount, meaning that founders can end up wasting lots of time and energy (Smith).

- Once founders have successfully raised funding, they are under pressure to deliver promised rewards to supporters on time, which can be challenging (Miller).

Equity crowdfunding allows founders to raise capital by selling equity to investors, but without giving up any control (Smith). Investors as equity holders receive a return on their investment and eventually a share of their portfolio company’s profits in the form of a dividends or distribution. In order to launch a successful equity crowdfunding campaign, founders should make sure to prepare an executive summary of their company, a pitch deck, terms of their fundraise, their business plan, and their company’s financials (McGowan).

Advantages of Equity Crowdfunding:

- Equity-based crowdfunding is likely to allow founders to raise larger capital than rewards-based crowdfunding.

- There are many accomplished investors on crowdfunding platforms who can contribute to the growth of startups (e.g. large amounts of capital and expert advice).

- Instead of raising capital from numerous investors, some equity crowdfunding platforms pool the funds raised into a single investment, making one point of contact for founders’ reporting duties.

Disadvantages of Equity Crowdfunding:

- Equity crowdfunding campaigns usually require founders to disclose their financials and business plans online for investors to evaluate, which some founders might not be comfortable with.

- Equity crowdfunding requires founders to give up some of their ownership and control over their companies to investors.

Examples of Successful Crowdfunding Campaigns:

- Oculus VR, an American VR hardware and software company, raised $2.4 million to make VR headsets through crowdfunding in 2012, which is ten times its original target, and was acquired by Facebook in 2014 for $2.3 billion.

- Critical Role, an American web series in which voice actors play a fantasy tabletop role-playing game, raised $4.7 million through crowdfunding in 24 hours.

Founders considering crowdfunding as a financing option should keep in mind the rules set by the SEC:

- “Require all transactions under Regulation Crowdfunding to take place online through an SEC-registered intermediary, either a broker-dealer or a funding portal"

- “Permit a company to raise a maximum aggregate amount of $1,070,000 through crowdfunding offerings in a 12-month period”

- “Limit the amount individual investors can invest across all crowdfunding offerings in a 12-month period”, and

- “Require disclosure of information in filings with the Commission and to investors and the intermediary facilitating the offering.”

Accounts Receivable financing

Receivables finance includes a number of different methods a business can use to raise funds against the amounts owed by customers from outstanding invoices, also known as its trade receivables or accounts receivable.

What is Accounts Receivable Financing?

Accounts Receivable (AR) financing is a type of financing in which a financier provides a company with capital related to its accounts receivable. AR is an asset account on a company’s balance sheet that represents any outstanding balances of invoices to be paid to a company by customers.

AR of large companies may be considered more valuable than those of small companies. Also, newer invoices are usually preferred over older invoices by financiers because they have longer collection shelf lives (Tuovila).

AR financing is often referred to as factoring, and AR financiers are often called factoring companies. There are two broad types of AR financing structures: asset sales and loans.

When AR financing is structured as an asset sale, a company sells its AR to a financier and the capital received replaces the AR on the company’s balance sheet as a cash asset. Depending on the terms, the company may receive up to 90% of the value of its AR (Tuovila). With asset sales, the financier bears the responsibility of collecting the AR. Therefore, some financiers may:

- Provide capital after AR is fully collected (Tuovila).

- Withhold some of the capital until AR is fully collected (Carbajo).

- Take a percentage of the paid invoices and place them into a reserved account, which can be used to cover any uncollectible (Carbajo).

- Include a full recourse clause which allows them to force companies to pay any invoices that are uncollectible after a specified period (Carbajo).

When AR financing is structured as a loan, a company simply receives a loan from a financier based on its AR instead of selling it; its AR may be used as collateral for the loan. AR financiers such as Fundbox offer AR loans as well as lines of credit to companies based on their AR (Tuovila).

Advantages of Accounts Receivable Financing:

- AR financing is a relatively quick and easy way to raise capital. Companies usually get quick access to capital without having to deal with long waits associated with many traditional methods of financing (Tuovila). Also, accounts receivable financing have relatively easy criteria and does not require any collateral (Carbajo).

- Companies “selling” their accounts receivable as assets do not need to worry about collecting them (Tuovila).

- Companies receiving accounts receivable loans may immediately obtain 100% of the value of their accounts receivable (Tuovila).

- Founders retain their ownership and full control over their companies (Carbajo).

Disadvantages of Accounts Receivable Financing:

- The costs of AR financing may be higher than traditional methods of financing, especially for companies with poor credit (Carbajo). For asset sales, companies may lose money from the spread paid for their accounts receivable. With a loan structure, interests may be high and failure to pay back within the predetermined period will only increase the total amount to be paid (Tuovila).

- In some cases, contracts can be very lengthy. Founders should try and negotiate the contract length that is suitable for their companies (Carbajo).

Revenue-Based Financing

RBF is most often used by small to mid-sized companies that do not qualify for traditional types of financing such as bank loans and venture capital (Parks).

What is Revenue-Based Financing?

Revenue-based financing (RBF), also known as royalty-based financing, is a type of financing in which investors provide a company with capital and receive a percentage of the company’s future ongoing revenues until a multiple of their principal investment has been paid (Parks).

Typically, payments are made monthly and the amounts vary based on the company’s monthly revenue (Tetreault)(Hayes). RBF is often considered as a hybrid between debt financing and equity financing.

The main difference between RBF and debt financing is that RBF does not require fixed payments and any interest to be paid on outstanding balance. RBF differs from equity financing as founders retain their ownership in their company (Hayes).

RBF is most often used by small to mid-sized companies that do not qualify for traditional types of financing such as bank loans and venture capital (Parks). Capital raised through RBF is generally used to scale the company by expanding efforts such as product development and hiring staff. Examples of companies that offer RBF include: Lighter Capital and GSD Capital (Tetreault). Also, many venture capital companies are getting creative with RBF methods for companies in the Software-as-a-Service (SaaS) industry today (Hayes).

Below are the general terms and requirements for RBF (Tetreault):

- Minimum monthly revenue requirements: $15,000 - $100,000

- Loan amounts: $50,000 - $3,000,000

- Gross margin required: at least 50%

- Payment terms: a fixed monthly percentage of gross (usually 3% - 10%)

- Total cost of capital (repayment cap): 1.35x - 3x the amount borrowed

- Interest rate: 18% - 30%

- Funding speed: 3 - 4 weeks

In addition, because investors see better returns on their investment the faster the company repays, they usually expect companies to have a plan to increase their business revenues and typically evaluate companies’ additional documents such as bank statements and investor decks (Tetreault).

Advantages of Revenue Based Financing:

- Qualifications for RBF are relatively easy to meet and the fundraising process is generally much easier and quicker than most traditional forms of financing (Tetreault).

- No interest is paid on an outstanding balance and there are no fixed payments; payments vary based on the company’s revenues (Hayes).

- Founders retain their equity and full control; investors do not have any direct ownership in the company (Hayes).

Disadvantages of Revenue-Based Financing:

- The costs of RBF are higher than that of conventional loans.

- RBF requires regular payments.

- Repayment period is shorter than most traditional forms of financing.